Weitere Informationen

Understanding the Landscape – Types of Crypto-tokens and Crypto-Ventures, and are they Regulated?

Fortunately for crypto-market participants, UK legislators and regulators have recognised the benefits of clear rules to promote the growth of the market, encourage innovation and ensure best outcomes for customers. The Financial Conduct Authority (FCA) remains the main regulator for crypto-ventures and crypto-tokens in the United Kingdom. To come under the FCA’s regulatory perimeter under the Regulated Activities Order (RAO), a crypto-venture must be 1) transacting in “specified investments”* , 2) undertaking a “specified activity” 3) operating as a business and 4) conducting activities in the United Kingdom. Where a crypto-venture meets all of these requirements, the business must obtain FCA authorisation before commencing the regulated activity. Failing to do so would constitute a criminal offense.

It is important to keep in mind that some crypto-tokens are not regulated investments and therefore crypto-ventures dealing with them would not require authorisation for their crypto-activities (although such ventures may still be regulated and require authorisation for other purposes). Likewise, authorisation would not be required if the activity is conducted by an individual, rather than a business, or if the activity is conducted wholly outside of the United Kingdom.

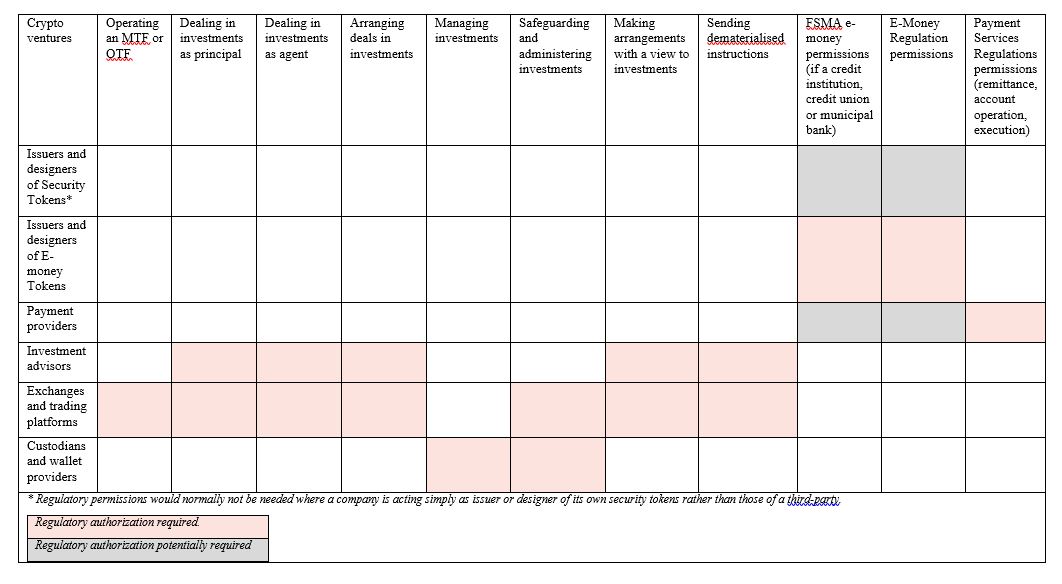

The table below sets out the four different types of crypto-tokens as specified by FCA and its guidance on whether they are regulated or not. It also covers the types of businesses associated with those tokens that would typically require FCA authorisation. Keep in mind that the FCA’s regulatory perimeter covers underlying specified activities rather than the overall business. For simplicity we don’t detail the underlying specified activities in the below table. Instead we list the businesses that are likely to be conducting activities that would be regulated. The underlying specified activities and permissions that could be required are set out in the table in Part 2 of this note.

In the Hot Zone: If a Crypto Venture is Regulated, what Rules Apply?

Basic Requirements

Even if the crypto-tokens are not regulated, if the business otherwise requires FCA authorisation, certain requirements will also apply to its crypto activities, including:

- FCA’s Principles for Business – e.g., fair dealing, acting in the best interests of customers, and exercising the requisite skill, care and diligence.

- Senior Managers and Certification Regime – Any individuals performing controlled functions within authorised firms will be liable for breaches with respect to their crypto-activities regardless of whether the tokens are regulated.

- Financial Promotion Rules – These are discussed in more detail below.

Regulatory Authorisations

If the business involves both regulated investments and regulated activities, it must obtain authorisation from the FCA before commencing activity. The permissions required could span a variety of regulations, including the Financial Services and Markets Act (FSMA), E-money Regulations and Payment Services Regulations. The business will need to obtain specific authorisation from the FCA for each of the regulated activities it intends to pursue, and failure to do so would constitute a criminal offense. In practice, these authorisations would all fall within one application and the requirements to be satisfied would overlap, including:

- A business plan setting out planned activities together with associated risks;

- A description of how the business proposes to fund its activities, including details of investors and funding sources; and

- Details of the corporate governance structure, including the board, senior management and governance arrangements

Financial Promotions

The financial promotions restrictions under FSMA apply to the marketing of regulated crypto-tokens irrespective of whether the crypto-venture requires FCA authorisation to operate, although various exemptions may apply. These restrictions also apply to unregulated crypto-tokens if they are advertised together with a regulated product or service. Generally, if the crypto-venture is unregulated but wishes to promote a regulated crypto-token, the promotion must be done in conjunction with a firm that has received FCA authorisation and has approved the communication. The content of the communication must also comply with the FCA’s rules on financial promotions, with the main requirement being that the promotion is clear, fair and not misleading. Marketing crypto-tokens in breach of these restrictions is a criminal offense.

One important point to keep in mind with respect to these rules and restrictions is that where a crypto-venture is FCA authorised but is marketing an unregulated crypto-token, such as Bitcoin, the venture cannot imply in the communication that its authorisation extends to the unregulated crypto-token.

Other Rules and Regulations

A variety of other regulations may also apply to crypto-ventures depending on the activities they undertake, including the Prospectus Regulation, Market Abuse Regulation, Money Laundering Regulations, Disclosure Guidance and Transparency Rules, Listing Rules, trading exchange/platform rules, and local laws in jurisdictions where an offer is made available internationally. These are outside the scope of this note, but should be kept in mind as they could be relevant.

Navigating the Minefield: How to Determine if You are Regulated

As a threshold matter, the FCA’s regulatory perimeter applies only where a business is dealing with regulated investments and conducting a regulated activity. It is important in the first instance to perform a thorough analysis of the crypto-tokens at issue to determine whether they should properly be considered regulated Security Tokens or E-money Tokens, or whether instead they would be considered unregulated Utility Tokens or Exchange Tokens. Once that assessment has been concluded, it is necessary to consider the nature of the business’ activities and whether they would be regulated as per the types of business and activities set out in the table in Part 2. Other factors to consider are whether the activity involves a business at all (vs being conducted by an individual in their personal capacity) and whether it is being conducted wholly outside of the United Kingdom, if either of these factors holds true then again the FCA’s regulatory perimeter would not apply.

Many crypto-ventures have unique business propositions that do not neatly fit into the FCA’s categories for regulated activities. Because of the rising numbers of these types of business, in 2014 the FCA launched Project Innovate, which provides direct support to innovative businesses to help them understand the FCA’s rules and processes. A crypto-venture may be eligible to submit a request for guidance to the FCA’s Direct Support Team where it can prove that its business model is genuinely innovative and likely to provide a benefit to customers, and that the firm has a genuine need for support.*

The Project Innovate support process is designed to be easily accessible and comprehensible, and it would be possible for firms to access and complete the guidance request materials even without the involvement of a solicitor, although professional advice may help a firm to more easily complete the submission and make a credible case with the FCA. If the FCA confirms that its regulatory perimeter does not apply, there would be no need to seek authorisation, and the reverse would apply where it disagrees with that assessment.

Conclusion

While the regulated status of crypto-tokens and crypto-ventures remains murky, the United Kingdom—in contrast to many jurisdictions—has attempted to put in place a framework that helps to clarify ambiguity and provide firms with support in the event there is any doubt. While the regulatory approach in this space likely will continue to evolve over time, there are at least some ground rules in place in the United Kingdom to help navigate this uncertain landscape. Where a firm falls within the FCA’s regulatory perimeter, it will need to seek authorisation for each of its regulated activities before commencing operations. Failure to do so is a criminal offense in the United Kingdom, making this an assessment of great import.

*1 The concepts of “specified investments” and “specified activities” are defined in the Financial Services and Markets Act 2000 (Regulated Activities) Order 2001 (SI 2001/544). For purposes of this note, we will use “regulated activity” and “regulated investment” to simplify the parlance.

*2 Stablecoins could be classified as Security Tokens, E-money Tokens or Exchange Tokens depending on the nature of the underlying asset and the stabilisation techniques used.

*3 The FCA’s Innovation Hub support materials are available here.