Overview

Market conditions, regulatory pressures, and technological advancements are converging to drive a new generation of deal structures as the healthcare landscape shifts to an innovative growth paradigm. And as evolving frameworks emerge, stakeholders are embracing creative investment opportunities.

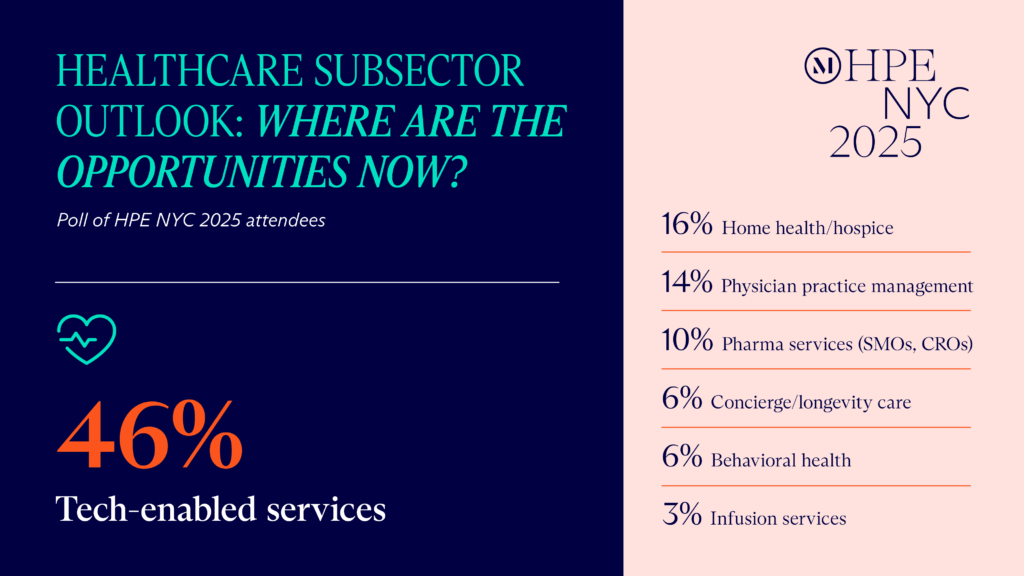

At McDermott Will & Schulte’s HPE NYC 2025, industry leaders explored some of these innovative strategies. We continue the conference conversations below with a review of the latest creative capital developments in the healthcare space.

In Depth

Novel pathways to value

- Bridging valuation gaps. Performance-based agreements and clever financing align valuation with performance in a selective buyer environment. These frameworks, along with strategic alliances and alternative liquidity paths – including continuation vehicles, minority recaps, and structured equity – require tactical structuring, tax optimization, particularized negotiations, and regulatory clearance. While not specific to one sector, these financing models reflect broader investor creativity in aligning value and performance.

- Private equity explores partnership opportunities. Demographic and regulatory shifts strain traditional industry economic models and require alternative means to address labor shortages, maintain profitability, and expand services. Private equity/health system partnerships are proving effective at meeting those needs when the parties share a fundamental alignment around incentives and a mutual understanding of how each will benefit from their partnership.

- Post-realization MedTech carve-outs provide value. Portfolio rationalization is a significant value generator as post-rationalization carve-outs offer investors access to innovation without the cost of full-platform premiums. Carve-outs allow global strategics to shed non-core units or finance technologies through partnerships with private equity. The process, however, is complex (and lengthy), requiring comprehensive diligence and robust transition services agreements between the parties.

- Biotech investment growth. Current biotech valuations may be particularly attractive to hedge funds. HPE NYC panelists shared some of the new approaches their firms are bringing to public and private investments, such as Private investments in Public Equity (PIPE) and hedging strategies (to manage portfolio volatility). The panelists also mentioned the potential for investment in Chinese biotech. Despite the potential legal and political challenges, they believe there is value to be found in Chinese biotech, particularly in the clinical trial phases.

- Increasing engagement in shareholder activism. Historically, most hedge funds faced with shareholder activism were likely to dispose of the asset rather than engage. Now, hedge funds may take it upon themselves to create change and unlock value through strategic pivots, asset sales, and capital reallocation while engaging management and emphasizing shared long-term goals.

Healthcare trends continue in new frameworks

- Joint venture participant range broadens. Recently, joint ventures in ambulatory surgery centers, labs, and imaging have been successful and are expected to grow. To illustrate, the panelists noted the lucrative partnership (in terms of profit and patient care) between a mammography company and a health system.

- Strategics investing in physician practices. Strategics continue to invest in the acquisition and consolidation of physician practices. They act as business enablers, providing the benefits of scale in technology, management, overhead, and overall efficiency while physicians maintain complete clinical autonomy and benefit from equity and wealth generation.

- Tech-enabled services mergers and acquisitions (M&A) activity. While broader M&A activity remains uneven, the panelists noted continued strength in tech-enabled platforms, decentralized trial capabilities, and demand for outsourced services. As platforms advance – with artificial intelligence, data, and omnichannel capabilities – into full-service commercialization, the market is rewarding scalability and integration. Anticipation and management of regulatory and compliance concerns is key, as the current M&A deal lifecycle is impacted by high-scrutiny environments in the United States and the European Union.

Custom legal structures enable investors to adapt

- Side pockets provide investment options. Hedge funds’ legal structures can significantly impact their ability to access private markets. Side pockets allow investors to maintain liquidity in the public market while participating in private deals. Traditionally, side pockets were designed to protect investors in the event an issuer went bankrupt or was delisted. More recent hedge fund structures, however, include side pockets from formation, allowing access to private deals with what is effectively a private equity fund within a hedge fund.

- Increased adoption of separately managed accounts (SMAs). SMAs are structured differently from traditional hedge funds; they are contractual relationships between investors and managers where the investor maintains ownership of the individual securities. Managers have access to the brokerage account, but their role is limited to buying and selling securities. SMAs have been gaining traction over the last several years, as they offer investors greater transparency and control.

Conclusion

Creativity continues to offer innovative, forward-looking investment opportunities throughout the healthcare industry.

As always, we look forward to discussing the details with our clients and partners. To explore any of these themes further, please reach out to a member of the firm’s Health & Life Sciences Group.