In Depth

Background

The SRT transactions, often referred to in the U.S. as “credit risk transfer” transactions or “synthetic securitizations” and in the EU legislation as “on-balance-sheet securitizations”, are a tool that enables banks to reduce their regulatory capital requirements (broadly speaking, the amount of capital they must lock in, corresponding to the riskiness of the lending portfolio).

Although banks have been using SRT structures since the 1990s, recent developments have significantly increased their popularity. At the outset, the phased implementation of higher capital requirements stemming from the Basel III reforms has pushed lenders toward alternative capital relief structures, which are cheaper than issuing additional equity and do not force the banks to reduce the existing loan portfolios. This trend was further reinforced by the increase in interest rates which increased the overall costs of issuance of any of the commonly issued regulatory capital products (such as AT1 or CET1 instruments), following the spectacular write-off by the Swiss regulator of all AT1 bonds issued by Credit Suisse in 2023.

SRT structures exist in different variants. They may be funded or unfunded, involving traditional or synthetic securitization, with or without the use of an SPV. The most typical SRT structure is set out below and involves a bank (an originator or protection buyer), an SPV (a securitization vehicle), and an investor (a protection seller).

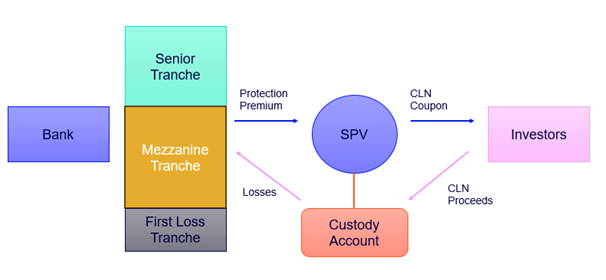

Illustration of a typical SRT structure.

In this structure:

- The bank selects loans to be included in the reference portfolio (usually comprising investment-grade corporate loans or those granted to small and medium-sized enterprises (SME) and divides them into three tranches: senior, mezzanine and first-loss tranche. The bank retains the senior and first-loss tranches.

- Regarding the mezzanine tranche, the bank enters into a financial guarantee or a credit default swap with the SPV, referencing the loans included in that tranche. Under that instrument, the SPV will compensate the bank for any losses stemming from these loans. In exchange, the bank will pay a protection fee to the SPV.

- At the final stage, the SPV issues a Credit-linked Note (the CLN) to investors (usually specialised credit funds, asset managers, public or multilateral development banks, or insurance companies) whose proceeds are held in a custody account and are used to fund the losses. The protection fee paid by the bank to the SPV is passed on to the investors as coupon payments under the CLN.

Contrary to traditional securitization, all portfolio loans remain on the bank’s balance sheet. However, for regulatory purposes, the mezzanine tranche with respect to the loans is treated as if removed from the balance sheet, thereby decreasing the capital the bank is required to hold against its loan portfolio.

Owing to regulatory constraints, only the mezzanine tranche can be utilized for the purposes of SRT. Among other things, these include the quantitative and qualitative criteria set out in Regulation (EU) 575/2014 (the CRR) and the risk retention requirements under Regulation (EU) 2017/2402 (the Securitization Regulation). Additionally, SRT structures remain subject to prior approval by the relevant competent authority, in compliance with the Public Guidance on the recognition of significant credit risk transfer (the SRT Guidance) issued by the European Central Bank (ECB).

New Securitization Rules Impacting SRT Transactions

The recent package of amendments to the EU securitization framework will introduce a number of changes to the existing SRT regime. Some of them aim to correct shortcomings identified by the European Banking Authority (the EBA) in the Report on SRT published in 2020. The EBA pointed to several flaws that contribute to market uncertainty, approval delays, and unjustified inconsistencies in the treatment of SRT securitizations with comparable characteristics across EU Member States. Other measures introduce additional incentives to the development of the SRT markets across the EU.

- New Harmonized Regulatory Approval ProcessAlthough the SRT approval process is currently governed by the SRT Guidance, the competent authorities of EU Member States have broad approval powers, including for certain SRT structures that do not satisfy the quantitative criteria under the CRR. This situation has resulted in significant differences between jurisdictions with varying local market practices.The amendments propose to harmonize the SRT approval process, to be enshrined in a new delegated regulation issued under the CRR, drawing on the fast-track process that is currently being implemented by the ECB. Further, the authorities would no longer have the power to approve non-compliant SRT structures (except for comprehensive reviews of complex and innovative transactions, to be further clarified in the delegated regulation).

- New Principle-Based Approach TestAs of now, in order to provide expected capital relief to the bank, the SRT needs to comply with the quantitative and qualitative tests set out in Articles 244 and 245 of the CRR. Often referred to as mechanical tests, they require, among other things, (i) the transfer of at least 50% of loans in the mezzanine tranche (in a three-tranche securitization), or at least 80% of the nominal amount of the first-loss position (in a two-tranche securitization), and (ii) that the capital relief obtained by the bank be less than the losses transferred. The new framework would replace these tests with a new principle-based approach (the PBA) test, requiring the bank to transfer at least 50% of the unexpected losses of the exposures of the underlying portfolio to investors. Additionally, to streamline regulatory assessment, the bank would need to submit a self-assessment demonstrating compliance with the PBA test, including under stress conditions, to be accompanied by a cash-flow model analysis. The details will be published in the delegated regulation.

- Increasing Access to SRT Transactions

- InsurersThe proposals will make several amendments to the Solvency II framework to incentivize insurers’ investment in SRT transactions.Among other things, the applicable risk factors for securitization investments will be reduced to align the insurance framework with the revised banking (CRR) rules. For instance, in securitizations qualifying as simple, transparent, and standardized (“STS“) under the Securitization Regulation, the prudential treatment of senior tranches will be aligned with the treatment of covered bonds. The STS label allows parties engaged in securitizations to apply lower capital requirements compared with non-STS securitizations.Further, the new rules will allow unfunded guarantees issued by insurers in the context of SRT transactions to satisfy the STS criteria (a possibility currently limited to specific public bodies and multilateral development banks).

- Multilateral Development BanksThe new regime will also increase the attractiveness of the SRT markets for multilateral development banks by waiving the risk retention and due diligence requirements under the Securitization Regulation for SRT securitizations whose first-loss tranche is guaranteed or held by such banks. This tranche will need to represent at least 15% of the nominal value of the securitized exposures.

- Investment LoansAs of now, for a securitization to qualify as an STS one, 100% of its underlying pool of exposures must consist of loans granted to SMEs. The amendments propose to lower this requirement to 70%, thereby opening the STS label and its benefits (i.e., lower capital requirements) to SRT transactions involving investment-grade corporate loans.

Assessment: Positive but Uncertain Change

The overall impact of the amendments on the development of SRT markets is expected to be unambiguously positive. On the structural level, the new regime would provide a streamlined approval process and greater market consistency, while offering banks necessary flexibility through the PBA test.

From a commercial perspective, the changes would increase access and the attractiveness of SRT structures, resulting in increased market liquidity. The proposed changes appear specifically tailored to support SRT market trends.

On one hand, insurers’ participation in SRT transactions remains limited, with their estimated share of the SRT market representing only 5% in 2023. Despite the fact that, as observed by the Commission, the insurance sector, “with trillions of assets under management,” remains a key institutional investor in the EU, SRT securitizations accounted for less than 1% of insurers’ portfolios in 2025. The amendments aim to incentivize EU insurers to engage in SRT transactions and, as a result, contribute to increasing EU banks’ lending capacity.

On the other hand, the participation of multilateral development banks in SRT transactions has been growing, with their share of the SRT market reaching 15% in 2023. European development banks, such as the European Investment Bank (EIB) (through its investment vehicle, the European Investment Fund (EIF)) or the European Bank for Reconstruction and Development (EBRD), are increasingly becoming significant players in the SRT markets. The Commission’s proposals reflect this trend and aim to encourage these institutions to continue expanding their activities in this area.

Controversy arises, however, around the need for reforms and their potential effects, with dissenting voices coming from within EU institutions, including bodies such as the EBA, the European Insurance and Occupational Pensions Authority (EIOPA) or the European Securities and Markets Authority (ESMA), as discussed in our previous article. More recently, this position was reinforced by Pedro Machado, Member of the ECB’s Supervisory Board, who expressed “fear that the proposals may have gone too far in reducing capital requirements for more complex transactions” and announced a detailed assessment of the measures in the upcoming opinion from the ECB. The extent to which, and when, the package will be implemented remains, therefore, uncertain.

Feel free to reach out to our team if you would like to learn more about the SRT markets or explore how you can benefit from the changes to the EU securitization framework.