Overview

Welcome to the fifth edition of the Private Markets Update, a report in which our cross-border, multidisciplinary team of private capital advisers shares insights on the latest trends emerging across global private markets. This year, these insights are enhanced thanks to the merger of McDermott Will & Schulte.

Throughout this report, you will find detailed commentary on some of the major themes impacting private markets, including the emerging opportunities in professional sports, data centers, and litigation finance. We are pleased to share updates on developments in hedge funds, real estate, and transatlantic restructuring while also looking at the regulations shaping cross-border M&A going into 2026.

As with previous editions of this report, we explore some of the latest data on private markets activity via our 10 Trends to Track list. These trends are deemed most pertinent as we move into a new year because they are topics of conversation among our clients and are high on the agenda of sponsors, investors, and other market participants.

Entering a new year is an opportunity to reflect on the past 12 months, which have not been easy for private capital providers. If 2024 was characterized by general election uncertainty (as huge swathes of the global electorate went to the polls), then 2025 was about coming to terms with the results of those democratic processes. A new US administration in the White House brought a trade policy shift that impacted deal flow in the first half of 2025 while new governments in the United Kingdom and Germany brought shifting fiscal priorities and new approaches to infrastructure spending. For fund managers, there was much to digest.

There remain many uncertainties going into 2026 and plenty of headwinds to navigate, but as the policy backdrop has clarified, so too has the appetite to transact. In the coming year, we expect exit activity to pick up, fundraising to strengthen, and sponsor-driven M&A to accelerate, with private capital on hand to support businesses as they continue to address liquidity challenges and shore up for a new phase of growth.

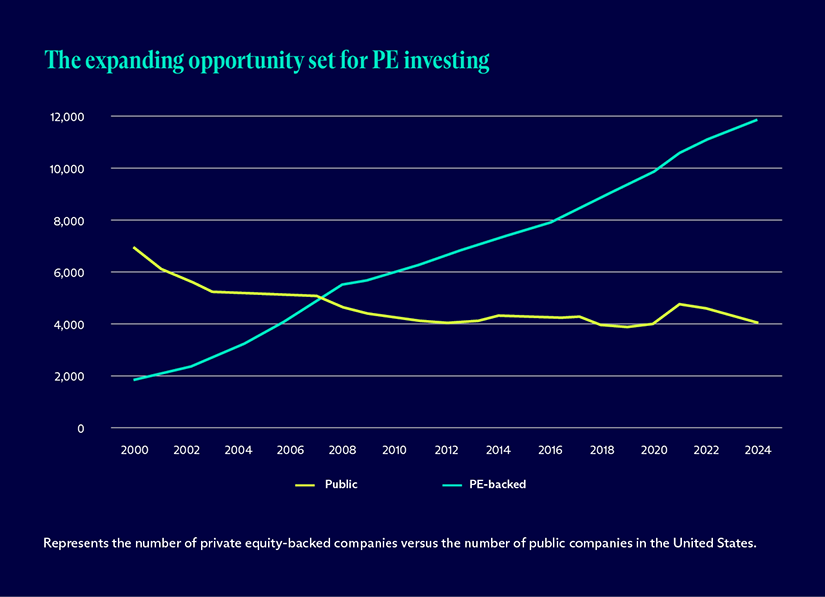

Trend 1: Private markets continue to expand

The amount of capital deployed into private funds continues to grow year-on-year. The world’s largest asset manager recently noted in their Private Markets Outlook, that private markets currently account for $13 trillion in assets under management, with that figure predicted to grow to more than $20 trillion by the end of the decade.

The growth of private markets is being fueled on the demand and the supply side. From a demand perspective, more companies are staying private for longer, with the number of businesses listed on US stock exchanges diminishing over time. Likewise, companies are increasingly turning to private capital providers for the funds they need to navigate liquidity challenges and finance growth, recognizing the ability of private funds to respond with agile, bespoke solutions.

On the supply side, more capital is looking to benefit from the returns on offer in private markets. Allocations from private wealth, insurance, pensions, and sovereign investors are all expected to materially increase in the latter part of the decade, as those investors seek access to the real economy and see private markets as the best way to achieve that exposure.

Source: morgansstanley.com

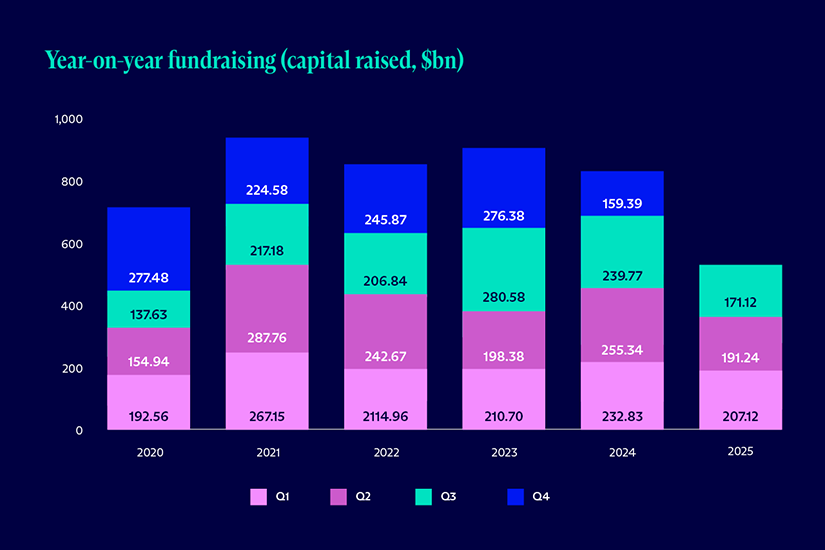

Trend 2: Fundraising remains steady

Fundraising for private funds has been difficult for the last couple of years, partly because of a lack of distributions to limited partners (LPs) that has inhibited their ability to reallocate to new vehicles. It is important to recognize the latest fundraising figures in the context of a cautious LP universe, too. Many large institutions already have meaningful amounts of capital deployed in private markets and have merely pressed pause to focus on DPI and consolidating relationships. Many have also been putting capital to work in structures that offer some liquidity, like evergreen funds and continuation vehicles. As such, given how active fundraising was from 2020 to 2023, it makes sense that the pace has slowed.

Data from Private Equity International shows that private equity fundraising in the first nine months of 2025 was lower than the same period in any year since the pandemic in 2020. The number of funds closed was also significantly lower, with 1,681 funds closed in the first three quarters versus 2,521 in the same period of 2024.

That said, certain strategies continue to raise well, such as healthcare, which is benefiting from its defensive profile and strong realization history. Industrials have also seen solid interest on the backs of supply chain, reshoring, and infrastructure trends. These areas of strength mean the market feels bifurcated rather than uniformly slow.

Additionally, we continue to see an extremely active market for independent sports and a competitive landscape around seeding arrangements. Several LPs are willing to make sizeable anchor commitments in exchange for economics, which continues to create opportunities, even in a slower fundraising backdrop.

With exits and secondaries improving, there is a solid argument that LP liquidity and pacing should normalize for private equity fundraising in 2026.

Source: privateequityinternational.com

For private credit, the story is somewhat different. According to Private Debt Investor data, a record amount of capital was raised for private debt funds in the first nine months of 2025, with funds totaling $252.7 billion (just above the $251.6 billion raised in the same period in 2021). By year end, 2025 could be a record year for private debt capital raising, driven to some extent by more challenging conditions in other parts of private markets.

Source: privatedebtinvestor.com

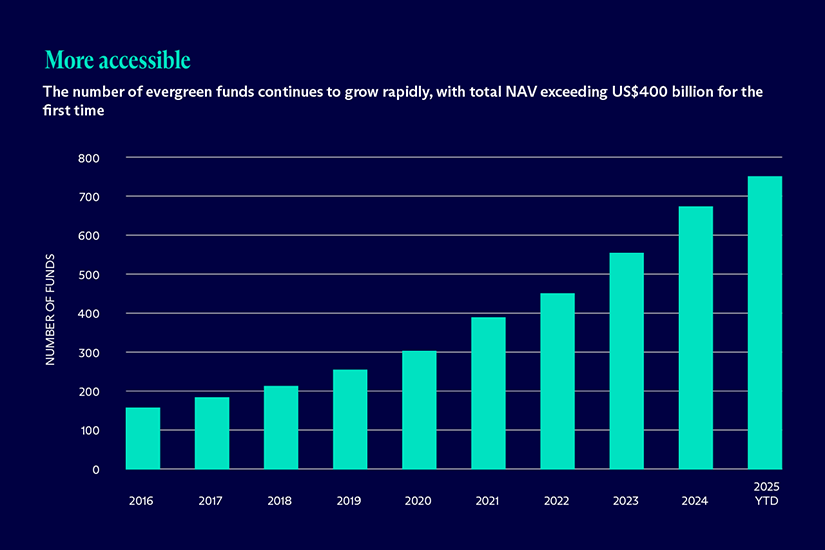

Trend 3: Democratization is gaining momentum

The private market funds investor base continues to evolve, with new fund structures being developed as asset managers seek to tap wealth investors looking to access the asset class. Our lawyers have pioneered the creation of evergreen fund structures over the past decade, helping to develop a range of open-ended, semi-liquid vehicles that offer investors continuous access and some form of liquidity while investing into illiquid asset classes.

The number of evergreen funds continues to grow rapidly, fueled not just by wealth investors but also by institutional investors attracted to periodic distributions and simplified tax reporting. These structures also help investors overcome some of the frustrations with traditional closed-ended drawdown funds, such as unpredictable capital calls and limited liquidity.

There is an ongoing push by governments to make private markets returns accessible to retirement investors in defined contribution plans, with US administration moving to open up private markets to 401(k) US pension plans in August 2026.

In 2025, the total NAV of evergreen funds topped $400 billion for the first time, according to data from the world’s leading asset manager.

Source: blackrock.com

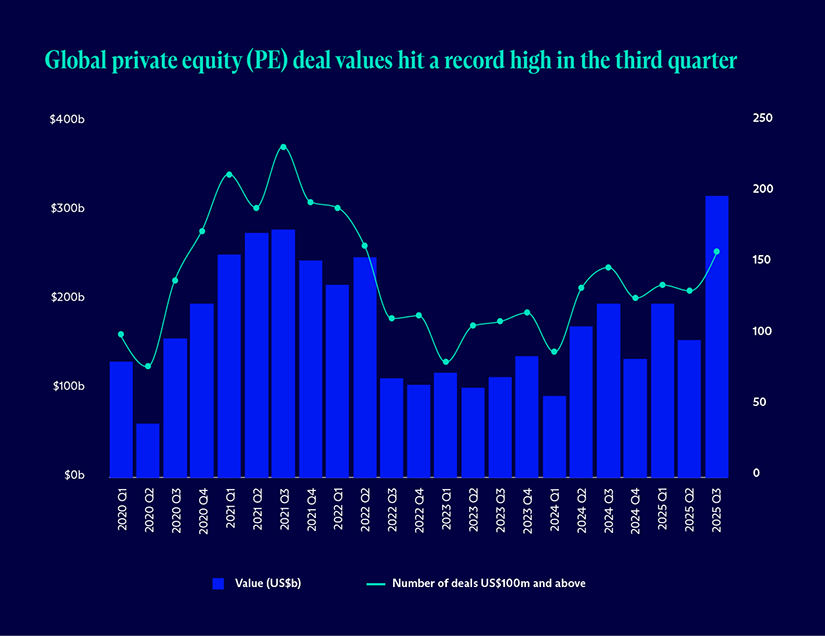

Trend 4: Transactional activity is improving

After several years of muted private equity transactional activity, there were clear signs of an upward trend in M&A in Q3 2025. According to data from EY’s Private Equity Pulse, private equity activity deal value reached a record $310 billion in Q3, the busiest quarter observed since the start of 2020.

Market participants have been poised for an uptick in deal activity for some time, after a mismatch in valuation expectations between buyers and sellers – compounded by macro and geopolitical uncertainty – had put the brakes on transactions.

Hopes of a rebound heading into 2025 were extinguished by the uncertainty surrounding trade policy changes in the United States, which had a global impact on risk appetite. But with those policies better understood by the summer, we have seen more willingness to transact as the year has played out. We are optimistic that the upward trend will continue as we enter 2026: The backlog of sale processes should start to unlock as sellers gain the confidence to bring assets to market.

Overall, the EY report records 156 deals valued at above $100 million in Q3, a number not seen since Q2 2022.

Source: ey.com

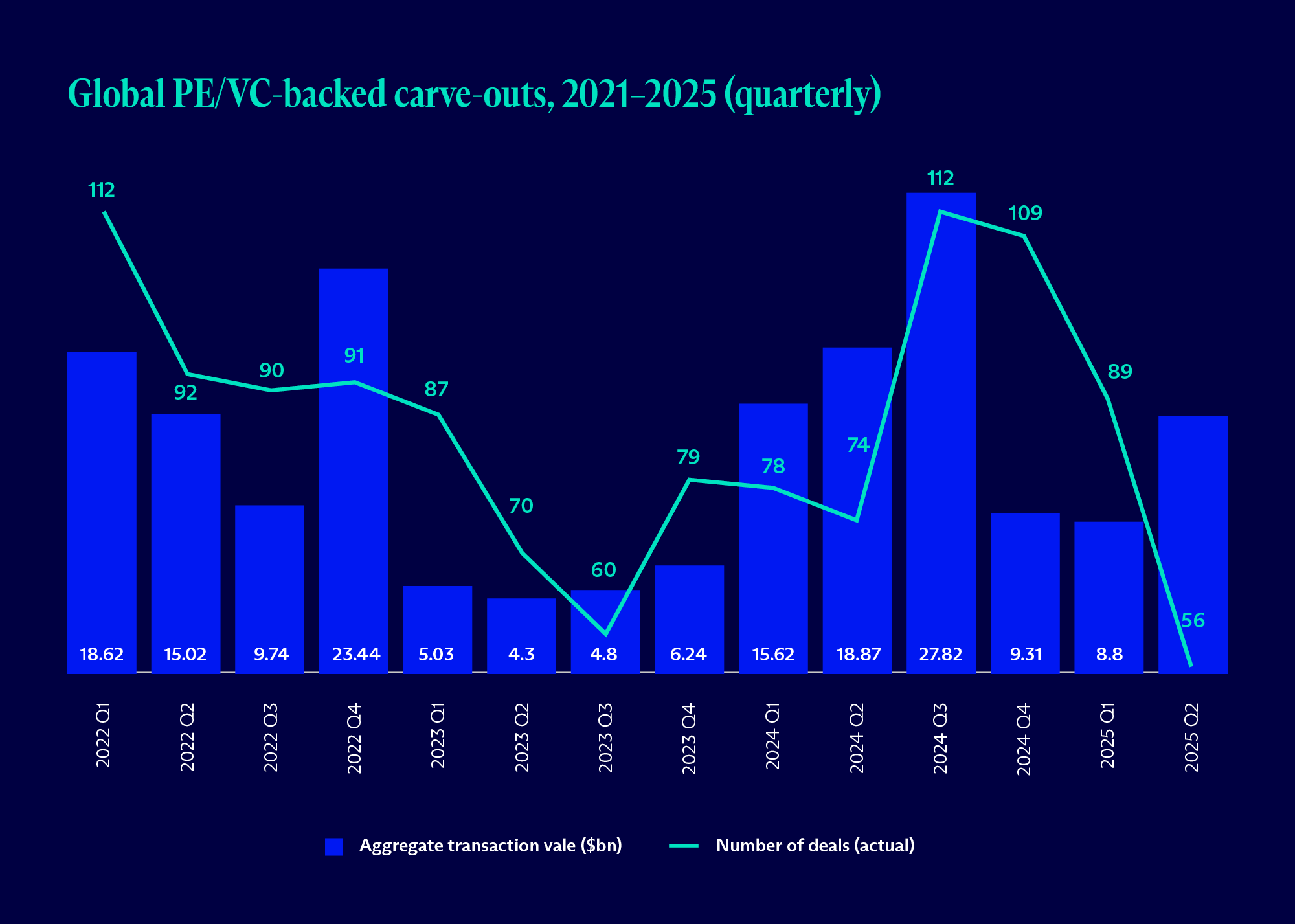

Trend 5: Carve-outs are growing in frequency and size

As corporates navigate several significant megatrends, including shifting international trade flows, energy transition, and the evolution of artificial intelligence (AI) and technology, many are looking to restructure around core business lines. As a result, we have seen an increase in corporate divestments, creating opportunities for private equity buyers.

Q2 2025 was one of the biggest three months for private equity-backed carve-outs for some time, with data from S&P Global recording $15 billion worth of deals done. That figure has been surpassed in only six of the last 14 quarters, and we anticipate the continued meaningful growth of carve-outs in both frequency and scale as companies divest non-core operations. For private equity firms looking to drive growth in a complex exit environment in terms of valuation multiples, carve-outs offer an attractive option.

The US and Canada saw the highest private equity carve-out deal value and volume in the first half of 2025, with 83 deals worth a combined $20.6 billion. By comparison, Europe saw just 47 deals worth $2.6 billion. Given that these deals are typically highly complex to execute because of the need to extract business lines and establish new operations from scratch, it is perhaps not surprising that they are primarily the domain of the largest private capital providers.

Most deals were done in the industrials sector, according to the S&P data, followed by energy and utilities – and those are markets where we expect to see more deal activity in 2026.

Source: spglobal.com

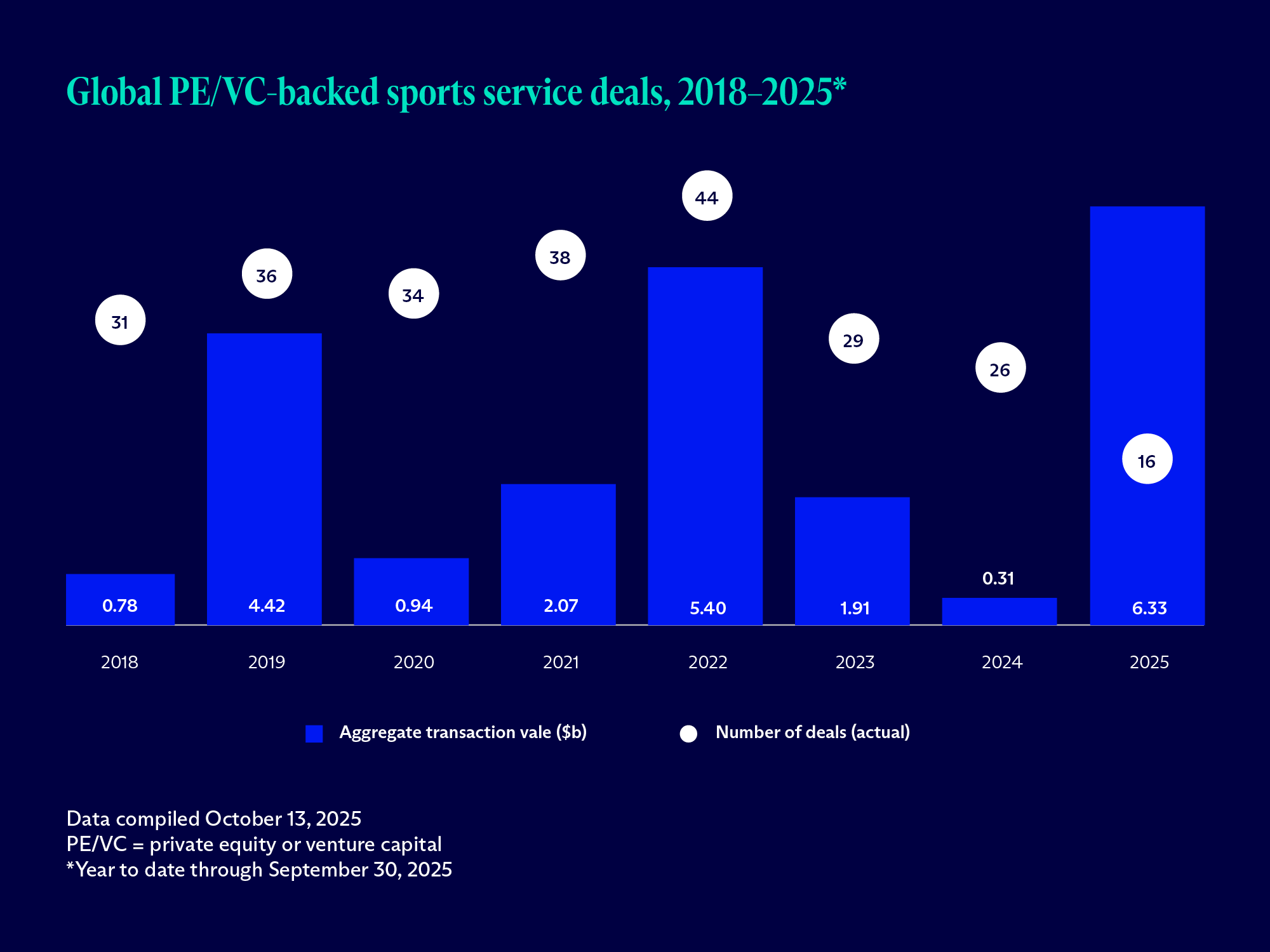

Trend 6: Private capital is moving into sports

Private equity’s appetite for investments in the sports world reached record heights in 2025. S&P Global data shows that aggregate transaction value hit $6.33 billion in sports and sports services for the first nine months of the year, exceeding previous 12-month highs.

Investors are attracted to professional sports teams, leagues, and services by escalating valuations that are being fueled by the growing value of media rights deals, appealing stability, recurring revenues, and loyal fan bases. In one of the biggest deals of the year, McDermott Will & Schulte assisted a buying group that included Aditya Mittal, William Chisholm, and Sixth Street Partners in acquiring the National Basketball Association team Boston Celtics for $6.1 billion. But plenty of opportunities are also arising in emerging sports.

Beyond the big four US sports of football, basketball, hockey, and baseball, we see investors increasingly looking to back teams in emerging sports like pickleball, lacrosse, padel, bull riding, and drone racing. Women’s sports also represent a large growth segment, as do various forms of football, such as flag football and spring football.

Historically, the domain of ultra-high-net-worth investors, relaxations of league shareholding rules, and growing awareness are expanding the sporting investor base to include private equity firms, current and former athletes, wealthy individuals, and even tech investors that can help leagues capitalize on new ways to monetize intellectual property.

Source: spglobal.com

Trend 7: Infrastructure deals are expanding

Infrastructure investment opportunities are increasing in scope as the demand for infra-like returns has seen funds broaden their horizons and the asset class widen.

The surge in AI and other emerging technologies is creating a huge demand for high-density data centers, with an increasing recognition that private capital will need to fill the infrastructure funding gaps across the world. Data centers require mammoth amounts of power and electricity grids are struggling to keep up, creating an investment opportunity in both digital infrastructure and the energy play while powering AI developments.

According to KPMG’s Pulse of Private Equity report for Q3 2025, infrastructure and transport deals attracted investments worth $126 billion in the first nine months, a three-year high with three months remaining.

The AI boom comes alongside a wider recognition among governments globally of the need to make meaningful infrastructure investments in areas like transport, defense, energy transition, and technology. Private markets are increasingly contributing to the flow of funding needed to support infrastructure needs, with asset-based finance growing more attractive to investors seeking less correlated, predictable contractual cashflows.

![Side-by-side graph visualizations fo Americas PE deal activity in (#) by sector (left) and ($B) by sector (right) [source: Pulse of Private Equity Q3'25 KPMG analysis of global private equity activity as of 30 September 2025. Data provided by PitchBook.]](https://d1198w4twoqz7i.cloudfront.net/wp-content/uploads/2025/12/18194103/McDermott_Private-Markets-Update-2026_Market-Analysis_Trend-8.png)

Source: assets.kpmg.com

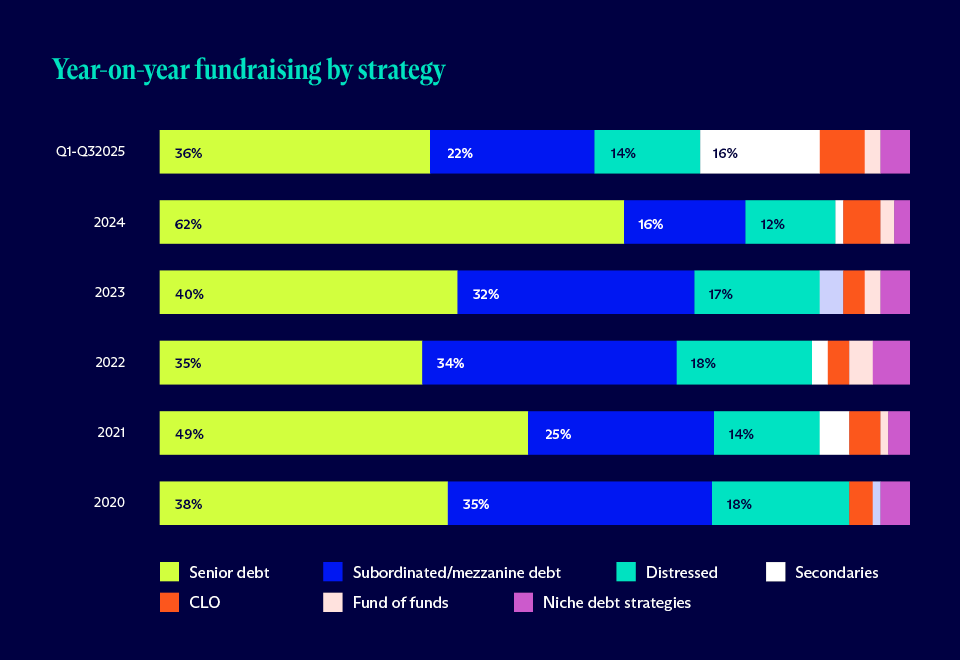

Trend 8: Private credit is both scaling and diversifying

Private credit funds remained active throughout 2025 despite M&A activity being at historic low levels. The asset class represented a bright spot in private markets fundraising and continued to dominate lending activity in credit markets in both the US and Europe. Borrowers looking for flexible, agile capital now increasingly opt to work with debt funds that can step in when traditional lenders or public markets are constrained.

As the asset class scales, private credit is diversifying and moving beyond traditional senior direct lending strategies. Funds are moving into new markets, embracing asset-backed lending strategies like litigation finance, NAV lending, consumer lending and trade finance, as well as opportunistic, distressed and secondaries strategies.

According to data from Private Debt Investor, 2025 witnessed a significant increase in fundraising for credit secondaries strategies, which represented 16% of private debt fundraising in the first nine months of the year. That total included some large fundraisings, with four funds closing over $5 billion in the first three quarters. This year is the first year secondaries have accounted for such a large portion of debt fundraising, with CLOs also growing and senior debt strategies down to just 36% of capital raising.

Source: privatedebtinvestor.com

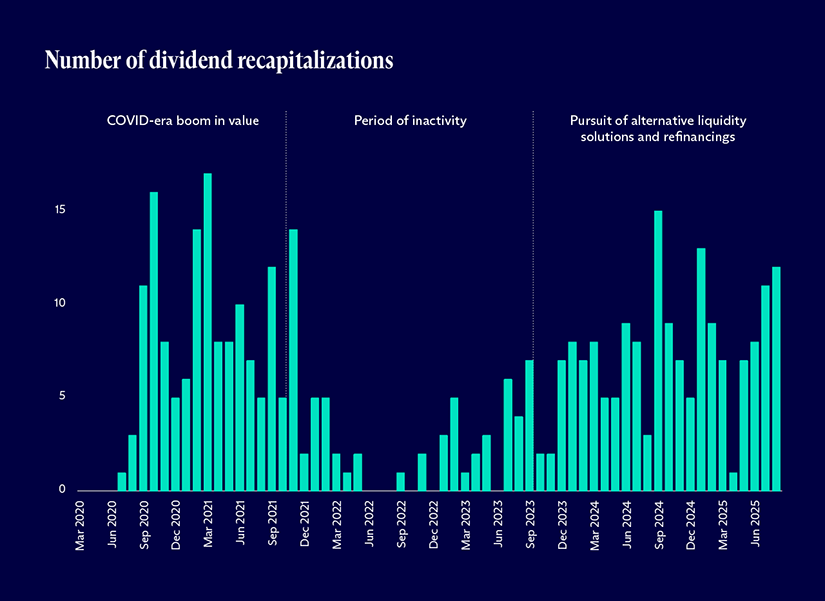

Trend 9: Dividend recaps rise in popularity

With credit markets strong and private equity firms anxious to return capital to investors, alternative exit strategies were one of the big themes of 2025. Continuation vehicles were a popular option for GPs tapping the secondaries market while the volume of dividend recapitalizations to drive DPI was also strong throughout the year.

Some reports indicated that as many as a third of firms were renegotiating pricing or structure and a similar proportion of portfolio companies were reassessing valuations in 2025. Faced with a challenging exit market, private equity firms were constrained in their ability to sell and saw recapitalizations as a good route for holding strong assets for longer while offering an element of liquidity to LPs.

The availability of capital and competition between private credit funds and the broadly syndicated loan market caused some downward pressure on spreads, making it even more attractive for sponsors to recapitalize performing portfolio companies.

Source: lincolninternational.com

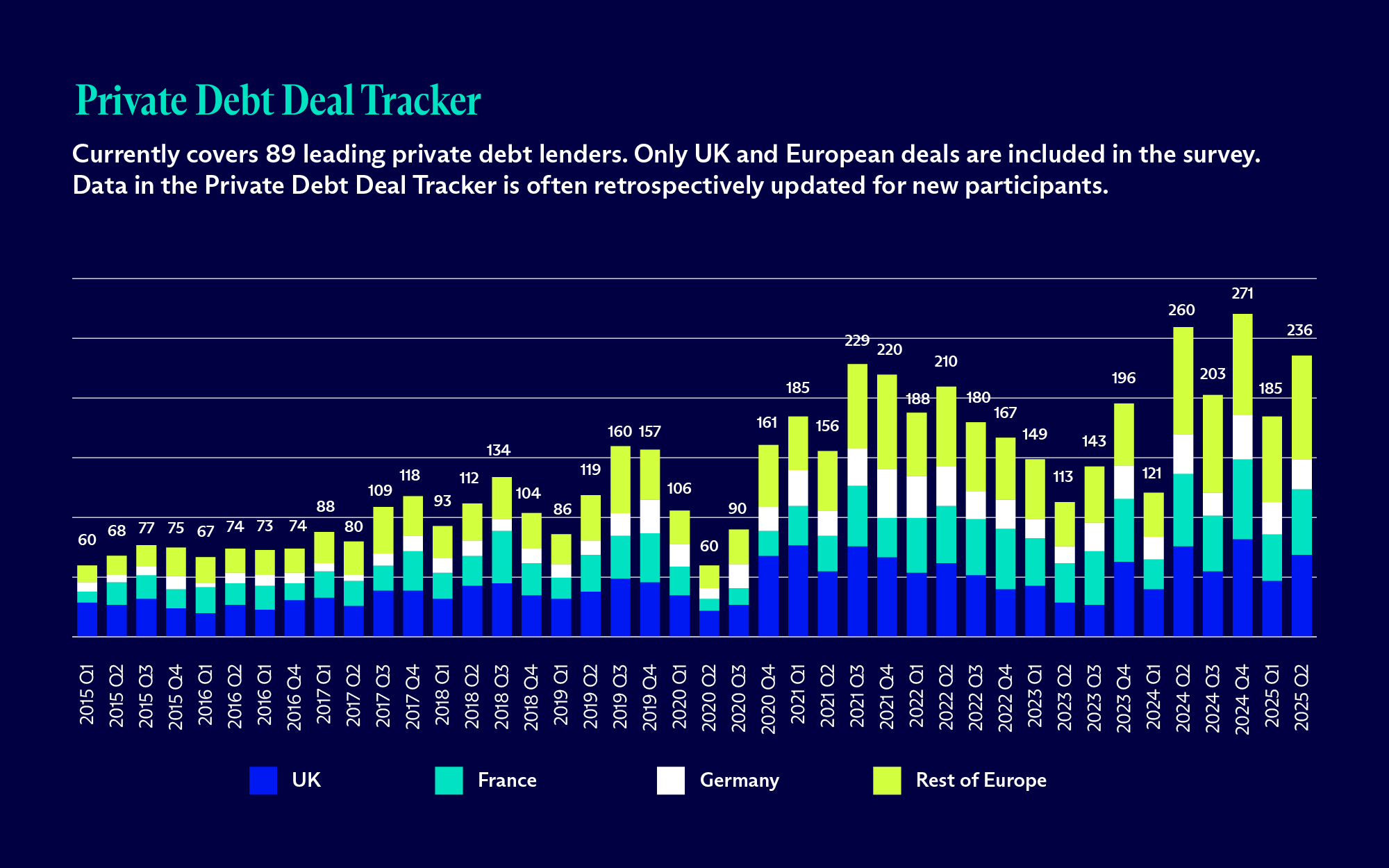

Trend 10: European private debt is busier than ever

The first half of 2025 was the busiest first six months of the year ever recorded for European private debt funds, with 421 transactions taking place across the continent versus 381 in the first half of 2024 and 398 in 2022 (the previous record).

Data from the Deloitte Private Debt Deal Tracker shows the European private debt market in rude health, with the UK, France, and Germany the largest markets with 116, 94, and 52 deals, respectively, in H1 2025.

Business, infrastructure, and professional services transactions accounted for one-in-three deals done, with technology, media, and telecoms the second most active sector for deployment, accounting for 21% of transactions in the first half of the year.

The size of private credit transactions also continues to grow in Europe. In the first half of 2025, €48.8 billion ($56.2 billion) in aggregate capital was deployed compared to €74 billion for the full-year 2024. Average deal size at the mid-way point stood at €205 million, up significantly from the €149 million average seen in 2024.

Source: deloitte.com