JANUARY – MARCH 2025: KEY THEMES AND TAKEAWAYS

UNITED STATES

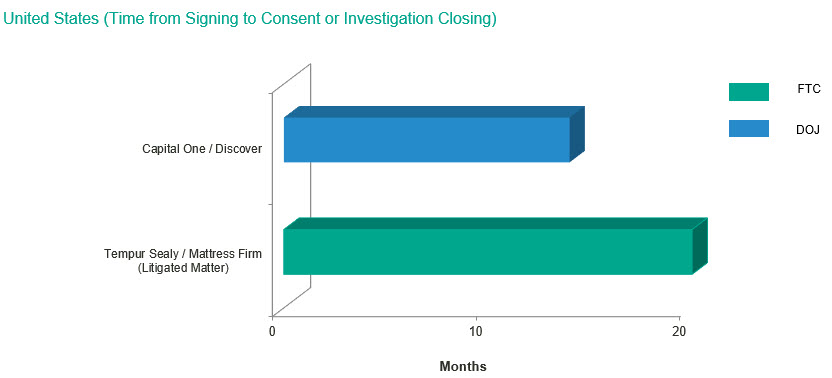

- FTC Loses Vertical Challenge to Tempur Sealy/Mattress Firm

On July 2, 2024, the US Federal Trade Commission (FTC) filed suit in federal court seeking to block a proposed $4 billion merger between mattress manufacturer Tempur Sealy International, Inc., and mattress retail chain Mattress Firm Group Inc. The FTC expressed concern that the merger would result in anticompetitive behavior from the companies, allowing Tempur Sealy to raise premium mattress prices for consumers through a customer foreclosure theory. The FTC alleged several vertical theories of harm, including Tempur Sealy foreclosing other mattress manufacturers, such as Serta Simmons or Purple from selling their products through Mattress Firm or disadvantaging them by limiting the purchase of their inventory, the floor space designated for their products, or the commissions paid to sales representatives when they sell rival mattresses. The agency also argued that the proposed remedies, including agreements to carry a certain percentage of mattress competitors’ products at Mattress Firm stores, were insufficiently limited in terms of timing and enforceability. In response, Tempur Sealy stated it planned to operate Mattress Firm as an independent chain, explaining that restricting mattress manufacturer competitors’ access to Mattress Firm stores did not make business sense, as it would substantially shrink Mattress Firm’s business.

On January 31, 2025, the US District Court for the Southern District of Texas denied the FTC’s motion. The court disagreed with the FTC’s premium mattress product market definition and found that Tempur Sealy’s ability to foreclose rivals was unsubstantiated, despite evidence in the parties’ documents that Mattress Firm was considered a ‘kingmaker’ in the industry. Even though the court found that Tempur Sealy would have the ability and incentive to foreclose rivals’ access to mattress shoppers, the court found that consumers and competitors would not be harmed because Mattress Firm’s in-store sales accounted for only 25% of all mattress sales in the United States. Furthermore, some rivals of Tempur Sealy did not even sell their products through Mattress Firm, opting to sell to department stores, furniture stores, online platforms, and via direct-to-consumer channels. For those competitors who sold through Mattress Firm, those sales accounted for only 9% of the manufacturers’ total sales. In fact, in 2021, Mattress Firm chose to stop selling Tempur Sealy mattresses, but Tempur Sealy’s sales for that time were not materially affected, discounting the assertion that Mattress Firm was a key retailer for mattress manufacturers. The district court found that the full record did not support the assertion that Mattress Firm was a critical sales channel that, if restricted, would result in foreclosure for Tempur Sealy rivals.

The district court also criticized the FTC economists’ model predicting a post-merger price increase for not taking into account elimination of double marginalization, or discounts passed onto consumers, that could result from the vertical integration of a manufacturer and its retailer. This serves as a reminder that courts are far more willing to recognize the elimination of double marginalization as an efficiency defense than the regulators were under the Biden administration. It remains to be seen how the Trump administration will deal with efficiencies from vertical mergers, but it is worth noting that the Vertical Merger Guidelines issued during the first Trump administration did credit elimination of double marginalization as a benefit of vertical deals. The court also concluded that the proposed remedies reasonably addressed anticompetitive concerns by promising to maintain supply agreements with and reserve space on the floor of Mattress Firm store for other mattress manufacturers and divesting a number of Mattress Firm stores to Mattress Warehouse. The court found that the proposed remedies would ensure that rivals of Tempur Sealy will have alternative retailers to sell through and would ultimately reduce both Mattress Firm’s market share and the likelihood of foreclosure by Tempur Sealy.

The outcome shows the difficulty in vertical challenges, especially ones based on customer foreclosure theories. Further, the district court’s opinion strengthens the viability of litigating the fix and the willingness of courts to view divestitures and other remedies as sufficient to cure potential anticompetitive effects.

- The Trump Administration Approach to Antitrust So Far

Despite the expectation that the second Trump administration would dismantle some of the anti-business antitrust policies or procedures established under the Biden administration, new agency heads FTC Chair Andrew Ferguson and Assistant Attorney General Gail Slater of the US Department of Justice (DOJ) Antitrust Division have stayed the course on several policies created by the previous administration, citing a need for consistency in enforcement. The agencies have retained the new Hart-Scott-Rodino (HSR) rules, which are far more burdensome on filing parties than the previous form and have led merging parties to agree to extended time-to-file provisions in merger agreements, now averaging around 20-25 business days to file. FTC leadership has stated that the level of detail required by the new HSR form has allowed enforcers to review deals and move quickly when there are no anticompetitive concerns. The agencies also have maintained and even cited the 2023 Merger Guidelines conceived by the previous administration, and plan to continue investigating novel theories of harm such as labor market issues.

Ferguson and Slater have also indicated their intention to focus on promoting dealmaking. They have brought back early termination to allow deals with no anticompetitive concerns to close without waiting the full 30 days for the waiting period to end and will seek to reduce bottlenecks around the HSR process. Additionally, the new administration has stated it will be far more receptive to settlement offers from merging parties allowing parties to cure anticompetitive issues to avoid injunction actions. Finally, Ferguson and Slater plan to protect average American consumers by focusing their efforts on the industries with which American consumers engage most often, including housing, healthcare, insurance, transportation, food, and entertainment.

Below is a chart of key antitrust policies, our assessment of the level of their importance to the Trump administration, and how the new approach differs from that of the Biden administration.

We are continuing to track new developments and provide timely updates on antitrust considerations coming out of the new administration. Get the latest information from our “Antitrust Under Trump: April 2025 Updates” client alert.

- Expansion of State Antitrust Laws

Increasingly, individual states have developed and implemented their own set of antitrust laws and regulations, applying these laws to anticompetitive actions by national and local companies that operate in their states. At several panels at the American Bar Association Antitrust Section’s annual spring meeting, state attorneys general (AGs) and representatives from those offices spoke of the states’ strong sovereign authority to enjoin anticompetitive behavior negatively impacting their citizens in the absence of government action, pointing out that federal antitrust laws may not protect local interests. States are also better positioned to coordinate with other state agencies that can inform antitrust investigations, such as California’s Office of Healthcare Affordability or Pennsylvania’s Department of Insurance, and can even leverage other sets of state laws in the antitrust context, such as charitable trust laws to review nonprofit transactions. As a result, a handful of states have been working toward creating new regulations or expanding and strengthening existing antitrust laws in their state.

For example, although Nevada has pre-merger notification requirements for healthcare systems, on March 21, 2025, state lawmakers introduced S.B. 218, a bill that would expand the notification requirement to all companies making HSR filings with the FTC and DOJ. In Washington state, lawmakers have introduced S.B. 5122, which requires parties with principal places of business in Washington or with annual net sales in Washington that are at least 20% of the HSR size-of-transaction threshold to submit a copy of their HSR filing to the state AG as well. S.B 5122 has passed the legislature and will go into effect on July 27, 2025. In New York, S.B. 335 proposes to amend the Donnelly Act, New York’s antitrust law statute, expanding the scope of the law by implementing an abuse of dominance standard and creating a rigorous pre-merger notification program. Introduced on January 14, 2025, S.B. 335 would require any transaction by a person doing business in the state which is HSR-reportable to be simultaneously submitted for review by the state AG, who would review each transaction for its impact on labor markets in New York as well as its impact on competition.

Over the last few years, Colorado, Illinois, Massachusetts, Minnesota, Oregon, Vermont, and Washington have also introduced antitrust laws, and Pennsylvania was considering such a law in mid-2024. Given the concern from states that the Trump administration will not be a robust steward of the antitrust laws, it will come as no surprise if more and more state merger control regimes are promulgated over the next four years to address perceived enforcement gaps.

EUROPEAN UNION

- The EC Published Its Competitiveness Compass, Signalling Future Changes to EU Merger Control

On January 29, 2025, the European Commission (EC) published the “Competitiveness Compass for the EU”, a flagship initiative aimed at shaping a coherent strategy to enhance Europe’s global competitiveness. Building on the findings of the Draghi Report on EU Competitiveness (September 2024), the EC outlines a strategic roadmap to foster growth and resilience within the EU over the next five years and establishes targeted measures under three core pillars: (1) reigniting innovation, (2) achieving decarbonization while maintaining industrial strength, and (3) reducing strategic dependencies through enhanced economic security.

As part of this broader initiative to close the innovation gap, in early March 2025, the EC announced an overhaul of its horizontal and non-horizontal merger guidelines to ensure that “innovation, resilience and the investment intensity of competition in certain strategic sectors are given adequate weight in light of the European economy’s acute needs.” This echoes the vision set out in the Draghi Report, which called for enforcers to consider the long-term innovation potential in strategic sectors, with a particular focus on defense and telecom, and a focus on strengthening European companies. This holistic review of merger policy is set to introduce a potential paradigm shift in EU merger control, aligning competition policy more closely with industrial and innovation objectives. In particular, the new merger guidelines will reflect the need to “keep pace with evolving markets and tech innovation.”

As Commissioner Teresa Ribeira has promised a consultative approach, a public consultation on both draft guidelines is expected in the second quarter of 2025, with further updates on the timeline to follow later this year. The revised guidelines are anticipated to be adopted for the fourth quarter of 2027.

1https://ec.europa.eu/commission/presscorner/detail/en/ip_25_339.

- EC Gathered Input for Upcoming FSR Guidelines

On March 5, 2025, the EC issued a call for feedback on the main objectives, scope and context of the forthcoming guidelines for the Foreign Subsidies Regulation (FSR).

These guidelines aim to clarify important concepts of the FSR, such as how to determine if a foreign subsidy distorts competition, the application of the balancing test, and the evaluation of distortions in public procurement procedures. Furthermore, the guidelines will cover the EC’s authority to mandate prior notification of concentrations or foreign financial contributions obtained in public procurement, even in instances that are below the notification thresholds established by the FSR.

Overall, the guidelines are intended to contribute to legal certainty, transparency and predictability in the enforcement of the FSR and assist companies in navigating its intricate provisions.

The EC has recently completed the initial stage, having closed its call for evidence on April 2, 2025. A draft version of the guidelines will be subject to public consultation at a later stage, with the final adoption of the guidelines planned prior to January 13, 2026, as mandated by the FSR.

UNITED KINGDOM

- The UK CMA Sets New Standards: Review of Merger Remedies and Release of Merger Charter

As part of its ongoing efforts to modernize and strengthen the UK’s merger control regime, on March 12, 2025, the UK Competition and Markets Authority (CMA) launched a comprehensive review of its approach to merger remedies.

Through this review, the CMA is seeking feedback from stakeholders on how to strike an appropriate balance between the use of different remedy types. Key areas of focus include remedy assessment (including when behavioral remedies may be appropriate), how remedies can be designed to preserve pro-competitive effects and other customer benefits, and how the remedy assessment process can be streamlined to enhance efficiency. Stakeholders have until May 12, 2025, to submit feedback. The CMA plans to use the insights gathered to develop detailed proposals, which will be published for consultation in autumn 2025.

Alongside this initiative, the CMA also introduced its new Mergers Charter. Designed first as a statement of intent, it outlines the principles that will guide its engagement with businesses and their advisors throughout merger investigations. The Charter is built around the “4Ps” principles – “pace, predictability, proportionality, and process” – and sets clear expectations for both the CMA and businesses to promote transparency, collaboration, and fairness. Consistent with the UK government’s intent to be open to foreign investment, the Mergers Charter appears to suggest a less aggressive review of mergers. The CMA expects to issue further guidance to support the Charter’s principles.

ENFORCEMENT IN KEY INDUSTRIES2

2 For the United States, the graphs include cases we are aware of in which an antitrust enforcement agency issued a second request at some point and the investigation remained ongoing during the quarter, the agencies accepted a consent order or issued a complaint initiating litigation against the transaction, or the transaction was abandoned after an antitrust investigation. For Europe and the United Kingdom, the graphs include cases where an antitrust enforcement agency issued a Phase II process or a clearance decision, or challenged the transactions, or the transaction was abandoned after an antitrust investigation.

SNAPSHOT OF SELECTED ENFORCEMENT ACTIONS3

3 These graphs are based on McDermott internal analysis and public press reports and filings. These graphs do not represent a complete list of all matters within a jurisdiction.

Notable US Cases

| PARTIES | AGENCY | CASE TYPE (CLEARED; CONSENT; CHALLENGED; ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

|---|---|---|---|---|

| GTCR BC Holdings, LLC / Surmodics, Inc. | FTC | Challenged: 13(b) preliminary injunction pending before the US District Court for the Northern District of Illinois |

Product market: Outsourced hydrophilic coatings, a critical input into lifesaving medical devices Geographic market: United States Merged entity would have more than 50% share; Herfindahl-Hirschman Index (HHI) increases surpass threshold for presumptive illegality |

Private equity firm GTCR sought to acquire Surmodics, the largest provider of hydrophilic coatings for medical devices such as catheters or guidewires, only a few years after GTCR acquired a majority stake in Biocoat, which is the second largest provider of these coatings. The FTC argued that the combined company would control more than 50% of the market for medical device hydrophilic coatings, and that due to the highly specialized nature of the products, new entrants are unlikely to appear because of the time and cost it would take to develop a competing product. Adhering to traditional antitrust principles, the FTC relied on presumptively illegal HHI concentration levels, the parties’ ordinary course documents, and commentary from other industry participants to bolster their arguments. The parties contest the FTC’s assertions, particularly the market definition. Surmodics produces coatings that are cured with ultraviolet (UV) light, while Biocoat’s coatings are cured with heat, which differentiates the products in terms of application. The parties allege that UV curing is not suitable for use in the interior of devices, while thermal curing is not suitable for use on devices that react poorly to high temperatures. The parties argue that their products are used on different kinds of equipment and are therefore complementary, not fungible. Notably, despite criticizing prior approval requirements imposed on merging parties by the previous administration and the constitutionality of Part III administrative courts, Republican commissioners agreed with their Democratic counterparts to demand that the parties obtain prior approval before making additional acquisitions in this industry, and to bring the case before an FTC administrative law judge in addition to filing a preliminary injunction in federal court. |

| PARTIES | AGENCY | CASE TYPE (CLEARED; CONSENT; CHALLENGED; ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

|---|---|---|---|---|

| Hewlett Packard / Juniper Networks | DOJ | Challenged; suit pending in the US District Court for the Northern District of California |

Product market: Enterprise-grade WLAN solutions, including wireless access points, hardware/software to manage the access points, and logistical support, which is sold to large institutions Geographic market: United States Merged entity would control more than 70% of the market, merger would increase HHI index by more than 250 points |

In the first federal merger challenge brought in President Trump’s second term, the DOJ sued to block Hewlett Packard Enterprise Co (HPE)’s acquisition of Juniper Networks Inc. (Juniper). The DOJ alleges that HPE and Juniper are the second and third largest providers of enterprise-grade wireless local area network technology. Such technology supports the connection between workplaces and employees or academic institutions and students for accessing and sharing information. The DOJ argued that over the last few years, Juniper has grown rapidly as a disruptive force in the market, which caused HPE to offer discounts and new product innovations in order to keep up. Asserting that HPE sought to acquire Juniper in order to quash competition, the DOJ relies on communication from HPE executives encouraging salespersons to “beat” Juniper and describing Juniper as a threat seeking to “unseat” HPE. In their answer, the parties point to other competitors in the market, the myriad procompetitive effects of the merger, as well as the reaction of industry analysts to the deal, as evidence that the transaction should be allowed to proceed. The parties argued that the transaction would accelerate innovation by pooling the resources of two strong companies, and would allow the companies to compete more effectively against the number one player in the market, Cisco. Industry analysts reacted with surprise to the DOJ’s market definition and stated that they did not anticipate the deal leading to a reduction in choice or price increases. Instead, they believe the deal would force Cisco to innovate and reduce prices as HPE did in response to Juniper. This case is ongoing. |

Notable European Cases

| PARTIES | AGENCY | CASE TYPE (CLEARED; CONSENT; CHALLENGED; ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

|---|---|---|---|---|

| Ansys, Inc. / Synopsys, Inc. | EC / CMA |

EC: Phase I; conditional clearance CMA: Phase I; conditional clearance |

Global markets for the supply of: (i) optics software; (ii) photonics software; and (iii) electronic design automation (EDA) software tools used for the design of chips |

On January 10, 2025, the EC cleared the acquisition of Ansys by Synopsys, subject to conditions offered by the parties, following a Phase I investigation. Ansys is a US provider of multi-physics simulation and analysis software, including EDA tools. Synopsys is a global supplier of EDA software, services and hardware used in the design of semiconductor devices, such as chips, as well as semiconductor intellectual property (IP). The EC identified potential competition concerns in several actual or potential overlapping activities in the market for the supply of optics software, photonics software, and EDA software tools used for the design of chips, and also raised issues about possible vertical and conglomerate concerns – specifically that the combined entity could bundle products or reduce interoperability between different EDA software tools or between EDA software tools and semi-conductor IP solutions for system-on-chip designs. To address the EC’s concerns, the parties offered structural remedies. These include the divestment of Synopsys’ optics and photonics software (including Code V, LightTools LucidShape, RSoft and ImSym) and Ansys’ register-transfer-level power consumption analysis software PowerArtist, subject to the EC’s approval of the purchaser. The UK CMA conducted a parallel review and cleared the transaction on March 5, 2025. Mirroring the EC’s concerns, the CMA found that the transaction gives rise to a realistic prospect of a substantial lessening of competition in the same three markets, which could potentially lead to less innovation, lower quality software, and/or higher prices. The CMA accepted the same structural remedies proposed to the EC. |

| PARTIES | AGENCY | CASE TYPE (CLEARED; CONSENT; CHALLENGED; ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

|---|---|---|---|---|

| International Paper Company / DS Smith Plc | EC | Phase I; conditional clearance | Manufacture and supply of (i) corrugated sheets in the North and West of Portugal, (ii) heavy-duty corrugated sheets in Northeast Spain, and (iii) corrugated cases in Northwest France |

On January 24, 2025, the EC cleared the acquisition of DS Smith by International Paper, subject to conditions offered by the parties, following a Phase I investigation. Both DS Smith and International Paper are vertically integrated paper and packaging companies with operations throughout Europe. The EC’s investigation identified competition concerns in a number of local markets in the EEA. In particular, the EC was concerned that the proposed transaction would significantly reduce competition in the markets for corrugated sheets in North and West Portugal, heavy-duty corrugated sheets in Northeast Spain, and corrugated cases in Northwest France. The EC’s investigation found that the transaction would have led to high combined market shares and increased market concentration, with limited competitive alternatives. This would likely have resulted in higher prices for customers in the affected areas. To address the EC’s concerns, the parties committed to structural remedies, including the divestment of five of International Paper’s plants in Europe: three in Normandy, France, one box plant in Ovar, Portugal, and one box plant in Bilbao, Spain. Subject to the approval of the purchaser(s), the EC found that these divestments would effectively remove the overlaps that raised competition concerns and mitigate potential vertical foreclosure concerns in the affected markets. |

| PARTIES | AGENCY | CASE TYPE (CLEARED; CONSENT; CHALLENGED; ABANDONED) | MARKETS / STRUCTURE (AS AGENCY ALLEGED) | SUMMARY & OBSERVATIONS |

|---|---|---|---|---|

| Aluflexpack AG / Constantia Flexibles GmbH | EC | Phase I; conditional clearance | Materials (chemicals, biochemicals, containers and packaging, metals and mining, paper and forest products) |

On January 29, 2025, the EC cleared the acquisition of Aluflexpack by Constantia Flexibles, subject to conditions offered by the parties, following a Phase I investigation. Aluflexpack is a manufacturer and supplier of flexible packaging solutions, including plastic and aluminum-based products. Constantia is a global producer and supplier of flexible packaging solutions, primarily made from aluminum. The EC’s investigation revealed that the proposed transaction would significantly reduce competition in the markets for sterilizable aluminum containers and lids used for wet pet food and certain human foods in the EEA. The combined entity would have held high market shares while facing limited competitive pressure from remaining suppliers. This raised concerns about potential price increases and reduced choice for human and pet food producers across Europe. To address the EC’s concerns, the parties proposed structural remedies, specifically the divestment of Aluflexpack’s entire sterilizable wet pet and human food packaging business in the EEA, including the assets and personnel of the Omial Novi production plant in Omiš, Croatia. Subject to the approval of the proposed purchaser by Constantia (MTX Group), the EC considered whether the divestiture of a stand-alone business would fully eliminate the overlap between the parties’ activities that raised competition concerns, by allowing the divested business to operate as a viable competitive force in the market on a lasting basis. Ultimately, the EC was satisfied by the proposed divestitures and cleared the acquisition. |