Flexible jurisdiction: The EU’s “referral up” and “referral down” toolkit in action

Jurisdictional allocation remains a defining feature of EU merger control, and recent cases have showcased just how flexibly the system can respond to the realities of modern dealmaking. Two contrasting referrals highlight both the strengths and the ongoing challenges of this approach: one “down” to a national authority, one “up” to Brussels.

A key trend in recent years is the increasing willingness of the European Commission to refer cases with purely national competitive effects to Member State authorities, even when the transaction meets the EU dimension thresholds. The Mehiläinen/Regina Maria Healthcare Group case is a textbook example: Despite the parties’ global scale, the deal’s impact was confined to Romania’s healthcare sector. The Commission’s decision to grant a full “referral down” under Article 4(4) EUMR reflects a pragmatic approach, ensuring that local markets are assessed by those with the best knowledge of their dynamics.

The Commission’s readiness to hand over jurisdiction signals growing trust in national enforcers’ expertise – especially in sectors such as healthcare, retail, and media, where market realities are often highly localized. For dealmakers, this means that even “big ticket” transactions may ultimately be reviewed under national rules and standards, with all the procedural and substantive nuances that entails.

Nevertheless, the referral system is not a one-way street. The Brasserie Nationale/Boissons Heintz case demonstrates how national authorities can invite the Commission to take over cases that, while local in scope, raise complex or sensitive competition issues. Here, Luxembourg’s request for a “referral up” under Article 22 EUMR was driven by concerns about market concentration and the need for robust, resource-intensive analysis. The Commission’s acceptance and its subsequent imposition of significant remedies shows that Brussels remains the forum of choice for cases with broader policy implications or where national authorities seek additional firepower.

National authorities are increasingly proactive in escalating cases to the EU level when they perceive a need for deeper scrutiny, cross-border coordination, or simply a more authoritative outcome. This trend is particularly pronounced in markets with entrenched incumbents, high entry barriers, or where remedies may have ripple effects beyond national borders.

The dual-track referral system is a strength of EU merger control, allowing for both local expertise and centralized oversight. However, it also introduces unpredictability: The same transaction could be reviewed under very different standards depending on the direction of referral, the appetite of national authorities, or even political considerations. Recent speeches by Directorate-General for Competition officials have emphasized the need for “coherent and efficient” allocation, but the practical reality is that forum shopping and procedural jockeying remain part of the landscape.

For merging parties, the message is clear: Jurisdictional strategy is now a core part of deal planning. Early engagement with national and EU authorities, careful mapping of potential competition concerns, and scenario planning for divergent outcomes are more important than ever. The key is to anticipate where the deal will land and to be ready for a review that is both local and European in character.

When remedies get real: From aerospace divestments to local distribution dynamics

Recent merger reviews by the UK’s Competition and Markets Authority (CMA) illustrate how competition authorities are sharpening their focus on the practical enforceability of remedies and how early engagement can make the difference between clearance in Phase I and a lengthy investigation. The Safran/Collins Aerospace transaction, reviewed in parallel by the Commission and the CMA, and the Schlumberger/ChampionX inquiry, assessed solely by the CMA, offer valuable insights into how remedies are evolving not just in substance, but also in structure, timing and execution.

In the aerospace sector, both the Commission and the CMA identified concerns in the market for trimmable horizontal stabilizer actuation (THSA) systems. These components are essential for aircraft stability and fuel efficiency, and the merger would have combined two of the few global suppliers. To resolve these concerns, Safran committed to divesting its North American THSA business, including sites in Canada, the United States and Mexico. The buyer, Woodward Inc., was preapproved by both authorities, as confirmed in the Commission’s decision published on October 10, 2025. The Commission emphasised that the buyer had to possess the technical capability and financial resources to operate the business as an effective competitor over time.

The CMA’s early involvement proved decisive. By working with the parties from the outset, the authority ensured that an effective remedy package and a credible buyer were identified before formal clearance. It accepted undertakings in lieu of a Phase II reference and imposed an upfront buyer condition. The CMA reviewed Woodward’s integration plans, including the relocation of certain manufacturing activities to Poland, as well as transitional service agreements, knowledge transfer arrangements, and buyer suitability criteria. This proactive engagement allowed the case to be cleared in Phase I. By contrast, the Commission also cleared the deal with commitments but delegated oversight to a monitoring trustee, reflecting a more traditional approach. The comparison highlights the CMA’s growing insistence that remedies must be operationally viable before clearance is granted.

The Schlumberger/ChampionX case, concerning oilfield services, reinforces this trend. The CMA accepted commitments in lieu of a Phase II investigation, having been closely involved throughout remedy design and buyer selection. It even required that the buyer be pre-approved prior to clearance, underlining its focus on ensuring that divestments would function effectively in practice. While the CMA maintains a clear preference for structural remedies, it is increasingly open to behavioral measures where these ensure that a structural divestment remains viable and achieves its intended effect.

There are several takeaways from the CMA’s approach to remedies. First, merger remedies are no longer just about what to divest but also how that divestiture will work in practice. Competition authorities are increasingly focused on the real-world implementation of remedies. Whether in aerospace or energy services, regulators expect merging parties to demonstrate that a remedy is not only conceptually sound but operationally workable and ready to go at the time of clearance. Early engagement and proactive remedy planning are now critical to achieving Phase I outcomes. Second, while structural remedies remain the benchmark, authorities are showing a greater willingness to accept supporting behavioral measures where these enhance the effectiveness of a divestment. The shift is toward remedy realism: Effective execution now matters as much as formal design. Where parties engage early and present credible, practical solutions, even complex mergers can obtain swift clearance.

EU and UK M&A activity: By the numbers

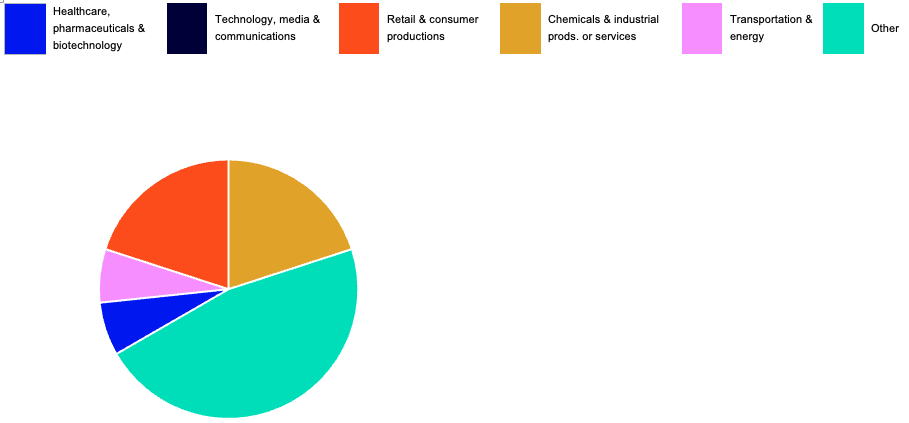

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

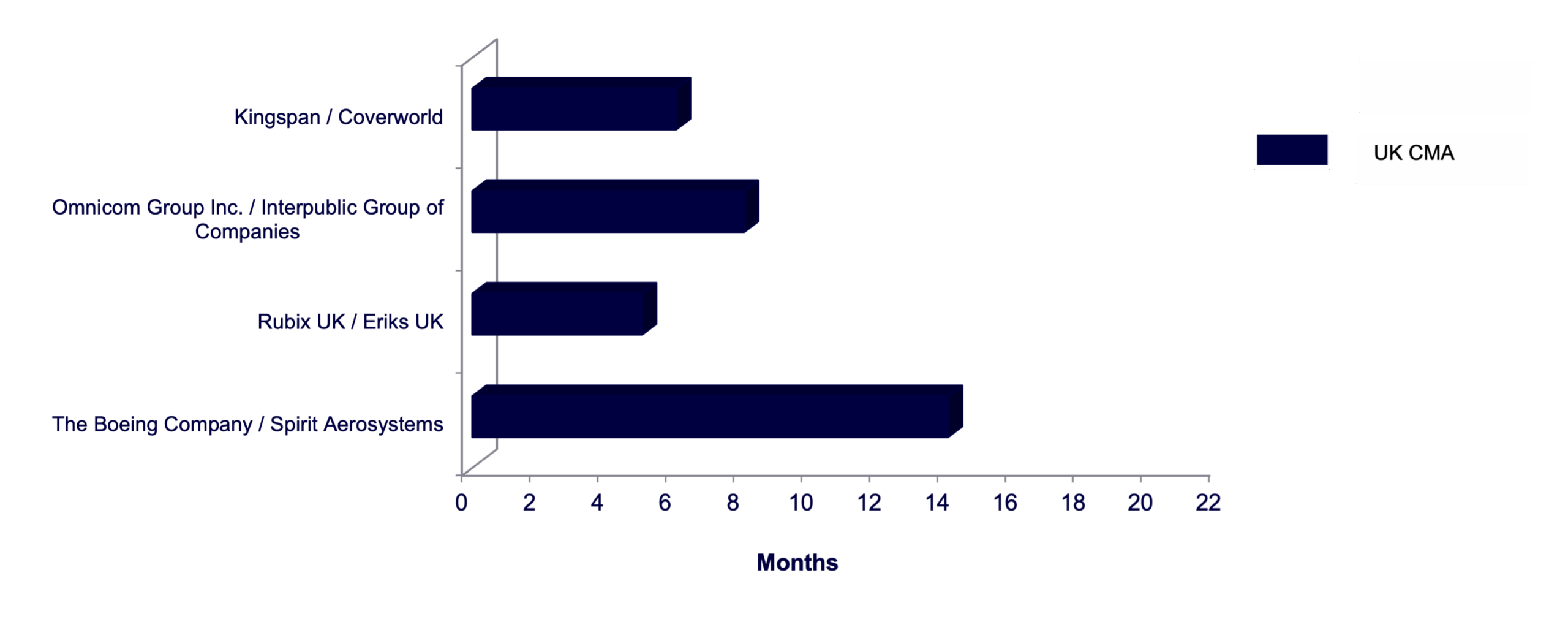

Time from signing to clearance