In Depth

European Union

Early and close engagement with the Commission results in clearances

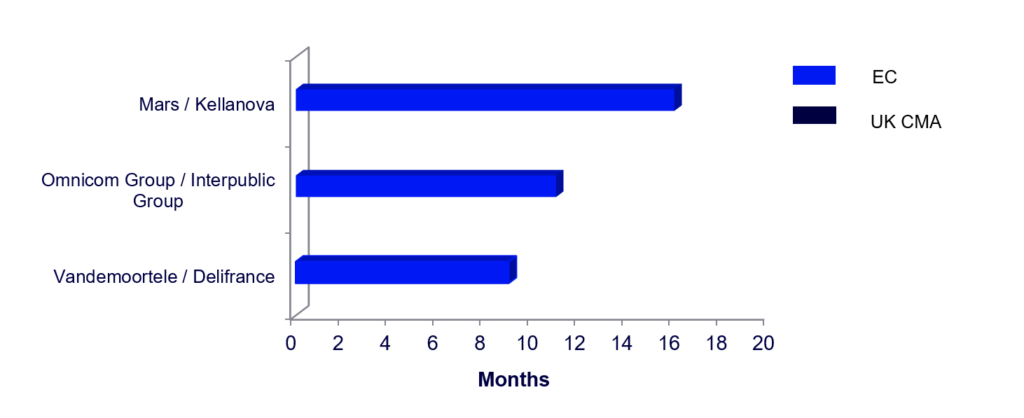

In the last quarter, the European Commission reviewed several complex transactions requiring significant regulatory scrutiny: (i) Mars’ acquisition of Kellanova, in which the Commission considered in-depth supplier power vis-à-vis supermarkets; and (ii) Omnicom’s acquisition of IPG, which was formally notified to the Commission in October 2024 and cleared in Phase 1, some 10 months after the deal was first announced.

In each case, the Commission eventually cleared the transaction, but only after requesting, reviewing, and considering thousands, if not hundreds of thousands, of documents submitted by the parties.

Unconditional clearance for Mars’ acquisition of Kellanova

One of the quarter’s most notable decisions saw the Commission unconditionally clear Mars’ acquisition of Kellanova in Phase 2 almost 16 months after deal announcement. The review focused on how the deal might affect bargaining dynamics with retailers for snack and cereal products. The Commission ultimately concluded that there was no credible risk of increased power leading to competitive harm, relying on the differentiated nature of the relevant product categories and the lack of evidence supporting increased brand loyalty or a “basket effect” on the part of consumers.

The investigation into portfolio effects highlights that the Commission will closely scrutinize transactions in markets where broad product portfolios play a large role and where products could be perceived as “must-stock.” Nevertheless, the unconditional clearance demonstrates that the Commission is unlikely to challenge under a portfolio effects theory without persuasive economic evidence and robust data.

Unconditional clearance for Omnicom’s acquisition of IPG

The Commission also unconditionally approved Omnicom’s acquisition of Interpublic Group (IPG), a merger that creates one of the world’s largest advertising and marketing services networks. The assessment found that existing competitive constraints – from players such as WPP, Publicis, and others – along with high customer mobility and relatively low switching costs, meant the deal was unlikely to significantly impede effective competition in the European Economic Area.

The parties did not formally file the transaction with the Commission until 10 months after deal announcement, after having obtained approval from multiple other jurisdictions. This transaction demonstrates that for complicated transactions parties need to spend a significant amount of time in pre-notification discussions with the Commission.

United Kingdom

CMA revises approach to remedies in year of streamlining merger control investigations

On December 19, 2025, the new guidelines for merger remedies, issued by the Competition and Markets Authority (CMA), took effect. The changes to the merger remedy guidelines are the latest installment in the CMA’s implementation of the “4Ps” framework – pace, predictability, proportionality, and process – which seeks to make merger control more transparent and business friendly. Key points include the following:

Behavioral remedies are more acceptable

While structural remedies remain the preferred option and the test remains the same (i.e., will the remedy be effective, and if so is the remedy proportionate?), the guidelines suggest a more open approach to behavioral remedies, especially if the CMA’s concern relates to specific activities and there is no other alternative remedy to “fix” an otherwise pro-competitive transaction.

Similarly, the CMA relaxed its position on accepting behavioral remedies during the first phase of the investigation. Behavioral remedies still must meet the “clear cut” standard, which requires that remedies must provide obvious and straightforward resolutions to competition concerns and be capable of ready implementation. However, the CMA highlights that early engagement on a remedy that aligns with established market practices and has a degree of market transparency, as well as the parties’ appointing a monitoring trustee, are all factors that increase the likelihood of the CMA accepting behavioral remedies early in the investigation.

Willingness to discuss remedies earlier in the review process

The CMA’s updated guidelines open the door for early, pre-notification discussions around remedies, with such discussions being “without prejudice” to the substantive analysis. Particularly with more-complex remedy packages that include carve-outs (as opposed to standalone businesses), the CMA seeks early engagement from the parties to provide measures to mitigate concerns such as the inclusion of an upfront buyer, the use of a monitoring trustee or independent expert to assess compliance, as well as potential alternative solutions should the remedy deal fall through.

The new guidelines bring to a close a year of realignment for the CMA and make the UK a much more deal-friendly environment.

After introducing new service standards that streamline the merger control process (reducing the average timeline from five to three-and-a-half months) and updating guidelines on jurisdiction and process, the CMA rounded out the year by publishing its latest annual merger investigation outcomes.

For calendar year 2025, the CMA considered 881 mergers (compared to 1,037 mergers in 2024), investigating 39 at phase 1 (compared to 38 in 2024), with only 4 referred to in-depth phase 2 review (compared to 6 in 2024). Of those phase 2 investigations, two were unconditionally cleared (compared to 2 in 2024), 1 resulted in acceptable remedies (compared to 2 in 2024), one was blocked (same as in 2024), and none was abandoned by the parties (compared to one in 2024). Overall, only 0.1% of all considered mergers were blocked or abandoned in 2025 (same as in in 2024).

EU and UK Q4 2025 M&A activity: By the numbers

Number of enforcement actions in key industries1

Snapshot of selected enforcement actions2

Time from signing to clearance